Chapter 6: Expenses and Budgeting

In Chapter 1, we introduced one of the most common challenges people have when trying to save. It’s the feeling that you don’t earn enough today to set aside money for the future. To address this concern, you could increase the amount of money you’re making. This can be done through working a second job, receiving a raise or completing freelance work. Efforts to increase your income can be very helpful to your financial success. There are resources available from free online courses to guides on how to ask for a raise. You can also offer freelance services through a range of communities.

However, you’ll likely find that as your income increases, your expenses do as well, leaving you back where you started. There’s a natural tendency to spend what you have available, which inflates expenses above what they need to be. If you have $5 for lunch, it’s typically possible to find a meal to meet your needs. But if you have $10 to purchase lunch, you’d likely not visit the same spot for a $5 meal.

The tendency to spend more as money becomes available is a large reason why many of us have trouble saving. While rewarding yourself for hard work is encouraged, it’s important to do so only after setting aside enough for the future.

In addition to working on your income, a more immediate and often effective option is to focus on what you spend. To demonstrate, let’s consider several ways you can rethink your expenses to help you spend less.

Pay Yourself for Spending Wisely

Imagine you’re going for dinner with a full wallet and an empty stomach. As you glance down the menu, you see lots of options at different prices. Once you’ve decided the most you’re willing to spend, step back and think about the situation with a different mindset.

Consider the difference between the most you’re willing to spend and the cost of the items on the menu. View it as the amount you’ll get paid to choose that item. For instance, if the most you’re willing to spend is $20 and a cheeseburger costs $14, the price difference of $6 is how much you can be paid to eat. By choosing the cheeseburger, you’ve saved $6 from what you had previously considered spending. It’s a perfect example of a dollar saved being a dollar earned.

Exhibit 15 – Rather than simply looking at the price of menu options, reframe the list and pay yourself while eating.

Receiving an immediate financial reward for wise spending is sometimes enough to sway your mind in the more economical direction. It’s hard to turn down ribs if the benefit is so far off, for instance a better retirement. By moving the reward to be in the same timeframe as the ribs, it’s easier for your mind to make a fair trade-off. The decision becomes, “Would you rather eat a rack of ribs, or be paid $6 to eat a cheeseburger?”

The simple reframing described above may be enough to change your spending habits. If it’s not, you can take the approach one step further. When you make the wise choice to spend less, transfer the difference from your chequing account to your savings account of choice. The tangible reward of seeing the impact of your decision should help you stick to your savings plan.

The High Cost of Convenience

Another way of thinking about expenses is to consider how much you’re paying for an hour of convenience. As an example, if you pay $5 to save fifteen minutes picking up a meal, you’re paying $20 an hour for your convenience. We often pay for services we can perform or products we can make without realizing how expensive it is. Some expenses are worth paying for, but others may be a bit harder to justify. If it costs you more to do it yourself, or you can better spend your time, then you should likely pay for the service. However, if it’s reasonable to do it yourself, then consider avoiding the expense.

Taking a taxi or ride-hailing service instead of public transit could cost you an extra $10 to save twenty minutes. Provided you’re not in a rush, it may be worth saving the equivalent of $30 an hour by taking public transit. Instead of treating expenses as necessities that often inflate with your income, look for where it makes sense to cut back. To think of it once again from the income perspective, you’re being paid to modify your spending habits.

Spending Your Time

A similar approach is to look at an expense as the number of hours you need to work to pay for it. If you earn $20 an hour, then the cost of purchasing a $40 shirt is comparable to working two hours. By taking the dollar value out of the picture, you can make your decision based on the actual trade-off. In the above example, you’re exchanging two hours of work for a new shirt.

Alternatives for Your Money

The final approach we’ll discuss is to consider alternatives for your money. Before making a purchase, briefly ask if there’s something else more deserving of that money. By getting the highest value out of your spending, you can lower your expenses without sacrificing your standard of living. It’s with this idea of getting the most from your money that we’ll move on to the topic of budgeting.

Budgeting: What It Is and Isn’t

One very important step in managing your spending is creating a budget. Before we discuss how to create a budget and what it should do, let’s briefly talk about what it shouldn’t do. A good budget shouldn’t lower your quality of life through constant guilt and pressure. It shouldn’t make you feel like you can’t afford to enjoy yourself when the opportunity arises. Instead, a good budget will allow you to spend guilt-free on what’s most important to you.

To understand the value of a budget, we need to agree on two facts. First, regardless what your income is, there’s a limit to the amount of money you can spend. Second, you have unique preferences and priorities that determine how you live your life. With these two facts in mind, a good budget will maximize the value you get from spending your money.

Let’s continue with the idea of making the most of your money and discuss the design of a successful budget. There are things in your life you can’t go without. For most, this includes a roof over your head and meals throughout the day. Regardless of what’s critical to your life, it’s important there’s always money available for them. A budget is meant to take your money and assign it dollar by dollar from top to bottom on your list of priorities. Recognizing a budget this way makes it a lot more attractive because you’re not saying no to this and no to that, but rather you’re saying yes to the things that are most important to you.

Not budgeting doesn’t mean you can spend your money on whatever you want because budget or no budget, at the end of the day when the money is gone, there’s no more to spend. With a well-planned budget, however, you’ll know you got the most from what you had available.

How to Create a Budget

Now that you’ve seen the importance of a budget and what its goals are, let’s discuss the steps to create one.

Calculate your income after subtracting taxes and savings.

Subtract your savings right away to ensure you get to your money first—as we discussed in Chapter 1.

List the items that bring you the most value for your money.

This could include rent, groceries, transportation, clothing, meals out, entertainment and many more.

Split your income in Step 1 across the items in Step 2.

Start with the most important and work your way down.

If you don’t have enough for an item on the list, then consider reducing spending elsewhere. The intention is to spend money where you’re getting the most value. Your expenses may be too high given your current income level, making it tough to include everything on the list.

The items on your list can be categorized as a required expense, discretionary expense or savings. Below are several examples of how to classify line items and a baseline of how much to spend on each category.

Required expenses, for example housing, groceries and transportation, should be less than 50% of your after-tax income.

Discretionary expenses, for example hobbies, travel and dining out, should be less than 30%.

Savings, for example retirement and loan repayment, should be roughly 20%.

As with any rule of thumb, the percentages are flexible depending on your unique circumstances and priorities. Through shifting around your spending, your ideal budget starts to form. You have now taken a set amount of money and made sure that every dollar will be used to bring you the most happiness possible.

Jennifer’s Sample Budget

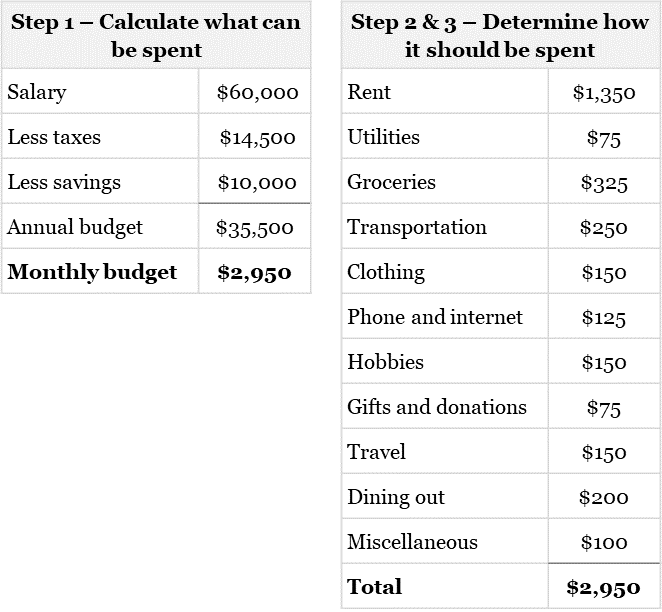

To see this process in action, we’ll create a budget for Jennifer, a thirty-year-old professional living in Toronto. Jennifer earns $60,000 a year. After paying $14,500 in taxes, Jennifer sets aside $10,000 toward savings and loan repayment. This leaves her with $35,500 a year to cover her expenses.

Exhibit 16 – The following budget shows how Jennifer’s money is spent each month and is based on her preferences and priorities.

Exhibit 17 – As we can see in Jennifer’s case, the 50%, 30% and 20% ratios provide a good starting point while allowing flexibility for her unique preferences.

Using Your Budget

A common misconception about budgets is that they’re written in stone. Many think that if there’s no money left in the entertainment bucket with five days left in the month that they’re out of luck. But that’s the type of limiting factor that often causes people to give up their budget or not start one in the first place. Therefore, the key to any good budget is flexibility. The plan was put in place when those categories were most important to you. If things change, change with them. Transferring money between buckets and readjusting your spending habits is only natural.

With that said, it’s still important to remember your budget is there to maximize the value you receive from your money. Remaining flexible doesn’t mean spending the month’s budget in the first two days because that isn’t going to maximize your return. It means that if you have $20 available for dinner out and you’d rather spend it on your favourite hobby, feel free. Don’t feel obligated to follow the budget dollar for dollar.

Sometimes unplanned expenses can have impacts on a budget you hadn’t considered. This is where the rainy day fund—mentioned in Chapter 5—comes into play. The rainy day fund is designed to protect against unexpected expenses by providing the money required in a time of need. Once you’ve paid for the expense, make sure to deposit savings to the fund until it’s back to the desired level.

It’s also important to remember that just because a dollar has been assigned to a bucket doesn’t mean it has to be spent. Possibly due to unexpected savings on a purchase or a friend leaving town resulting in no dinners out, you may find yourself with extra money at the end of the month. This money can be used as you please. You may add it to your savings if you’re already happy with the money you’ve assigned for the next month. If not, then perhaps a split between entertainment and dinners out would provide the best value for your money. Whatever bucket is decided, just remember that you can always apply current budgeted money to a future date if desired.

Final Thoughts

Creating a budget or, more broadly, any financial plan is about balance between today and tomorrow. Setting aside 50% of your money for the future at the expense of enjoying yourself today is just as bad as not saving at all. The goal is to set aside enough money to maintain your standard of living throughout your life. Celebrate the money you’ve earned as you spend it on things that bring you happiness, and ensure you can continue to do that in the future by setting aside an appropriate amount in savings.

A budget is meant to increase your quality of life by assigning your money to the most important expenses and ensuring you’ll have enough money to last. By following the steps outlined above to develop a personal budget, you’ll be better able to set money aside for the future while continuing to enjoy your day-to-day life.

Key Takeaways

Lowering expenses is often more effective than raising your income if you want to save more.

Set up a budget to assign your money to the most important items in your life.

Saving money is a balance of enjoying your life today and in the future, don’t sacrifice one for the other.

You can download a budgeting template with a 5 step walk through to help you get the most from your spending.

This blog is a duplicate of the recently self-published book The Snowman’s Guide to Personal Finance available for purchase here.